A credit utilization ratio is an important credit number. It shows how much credit you are using. It also shows how much credit you have left. Lenders look at this number when reviewing your credit. Every credit card has a credit limit. This is the maximum amount you can spend.A lower ratio is usually better. It shows that you are not using too much credit. This can help your credit score. A higher ratio may lower your score. Firstly you understand how to use the credit and how to improve an existing score.

What Is a Credit Utilization Ratio?

A credit utilization ratio is a percentage. It shows how much credit you are using. It compares your balance to your credit limit. This number is important for your credit score. Lenders pay attention to this number. They use it to understand your credit habits. A lower ratio usually looks better. It shows that you are using credit responsibly. A higher ratio may be a warning sign. It can suggest that you depend too much on credit. This may lower your credit score.Your ratio can change every month. It goes up when you spend more. It goes down when you pay your balance.

How Does Credit Utilization Ratio Work?

Many people ask, how does credit utilization ratio work?

The ratio measures how much credit you are using. The lower ratio is usually better for your credit health. Every credit card has a credit limit. This is the maximum amount you can spend. When you use your card, part of that limit is used and your utilization ratio shows how much of the limit is currently being used. Lenders look at this number carefully. It helps them understand your credit habits. A lower ratio usually looks better. It shows that you are using credit responsibly. A higher ratio can be a warning sign. It may suggest that you depend too much on credit. This can sometimes lower your credit score. Your utilization ratio changes whenever your balance changes. If you spend more, the ratio goes up. If you make a payment, the ratio goes down.

For example:

- Credit Card Balance: $500

- Credit Limit: $2,000

Credit Utilization Ratio:

($500 ÷ $2,000) × 100 = 25%

This means you are using 25% of your available credit.

The lower your utilization ratio, the better it generally looks to lenders.

Credit Utilization Ratio Example

Let’s look at another credit utilization ratio example.

| Credit Limit | Balance | Utilization Ratio |

| $1,000 | $100 | 10% |

| $2,000 | $500 | 25% |

| $5,000 | $1,500 | 30% |

| $10,000 | $5,000 | 50% |

In these examples, the person using only 10% of their available credit is generally viewed more favorably.

Lower utilization often supports a healthier credit profile.

How to Calculate Credit Utilization Ratio

Many consumers want to know how to calculate credit utilization ratio. So I will explain how to calculate the ratio. Firstly you see the formula:

Credit Utilization Ratio = (Total Balance ÷ Total Credit Limit) × 100

Example:

Suppose you have:

| Credit Card | Balance | Credit Limit |

| Card A | $300 | $1,000 |

| Card B | $700 | $2,000 |

| Card C | $500 | $2,000 |

Total Balance = $1,500

Total Credit Limit = $5,000

Calculation:

($1,500 ÷ $5,000) × 100 = 30%

Your credit utilization ratio is 30%.

Does Credit Utilization Affect Credit Score?

- It is one of the most important factors in many credit scoring models.

- A high utilization ratio can lower your credit score.

- A low utilization ratio can help improve your score.

- Credit scoring systems often view lower utilization as a sign of responsible credit management.

- Using too much available credit may indicate higher financial risk.

- This is why keeping balances low is often recommended.

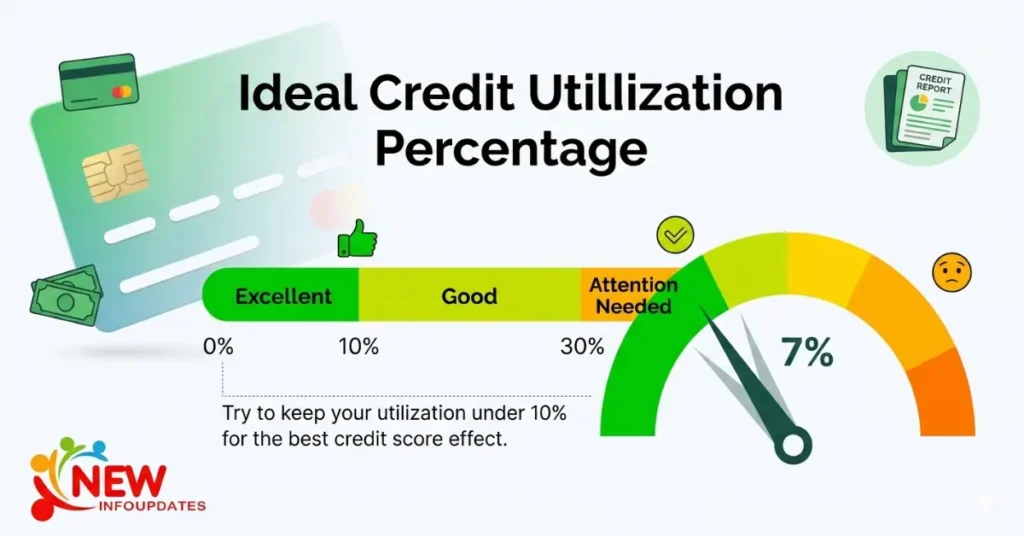

Ideal Credit Utilization Percentage

The ideal credit utilization percentage is generally below 30%. So your credit limit is 30% below. A lower percentage is usually better for your credit score. Many credit experts recommend keeping your utilization even lower. Staying below 10% is often considered excellent. It shows lenders that you use credit responsibly and do not rely heavily on borrowed money.

Here is a general guideline:

| Utilization | General interpretation |

| Below 10% | Excellent / often best for scoring |

| 10%–30% | Generally good |

| 30%–50% | Fair; may start to hurt scores |

| Above 50% | Poor; higher risk signal |

Many people with excellent credit scores maintain utilization below 10%.

Practical target

- Stay below 30% overall. Treat this as the minimum healthy target.

- Aim for 1%–9% before statement closing dates. This is often the strongest scoring range while still showing active credit use.

- Avoid 0% all the time if you are trying to demonstrate active usage. Some scoring models prefer seeing a small reported balance rather than no activity on every revolving account.

- Pay down balances before the statement closes if you can. That is usually the balance that gets reported.

Tips to Lower Your Credit Utilization Ratio

If your utilization ratio is too high, consider these strategies:

- Pay down credit card balances.

- Make payments more frequently.

- Avoid unnecessary purchases.

- Request a credit limit increase.

- Keep old credit accounts open.

- Use multiple cards responsibly.

- Check your balances regularly.

- Create a monthly spending budget.

Common Credit Utilization Mistakes

Avoid these common mistakes:

- Maxing out credit cards.

- Closing old credit accounts.

- Carrying high balances month after month.

- Ignoring credit card statements.

- Applying for excessive new credit.

These habits can increase your utilization ratio and potentially hurt your credit score.

Benefits of a Low Credit Utilization Ratio

Keeping utilization low offers several advantages:

- Higher credit score potential.

- Better loan approval chances.

- Lower borrowing risk.

- Improved financial flexibility.

- Better interest rate opportunities.

- Stronger credit profile.

Good credit habits often lead to better financial opportunities.

Conclusion

A credit utilization ratio is important for credit health. It shows how much available credit you are using. This number can affect your credit score. Understanding how a credit utilization ratio works is important. Looking at a credit utilization ratio example can make it easier to understand. Learning how to calculate a credit utilization ratio can help you track your credit use. Many people also ask if credit utilization affects a credit score. The answer is yes. Most experts recommend keeping your utilization below 30%. Lower percentages are often even better. Keeping balances low can help.