FICO scores and credit scores are very helpful for beginners. These scores may look like difficult money numbers, but they are actually simple once you understand them. A credit score shows how well a person uses borrowed money. A FICO score is one type of credit score used by many lenders. Both scores help banks decide if someone is responsible with money. Good scores can make borrowing easier, while poor scores can create problems. Credit scores are built from everyday money habits. Using too much credit at one time can lower scores. Small careful spending is usually better. Good habits help scores grow slowly over time.

What Is a Credit Score?

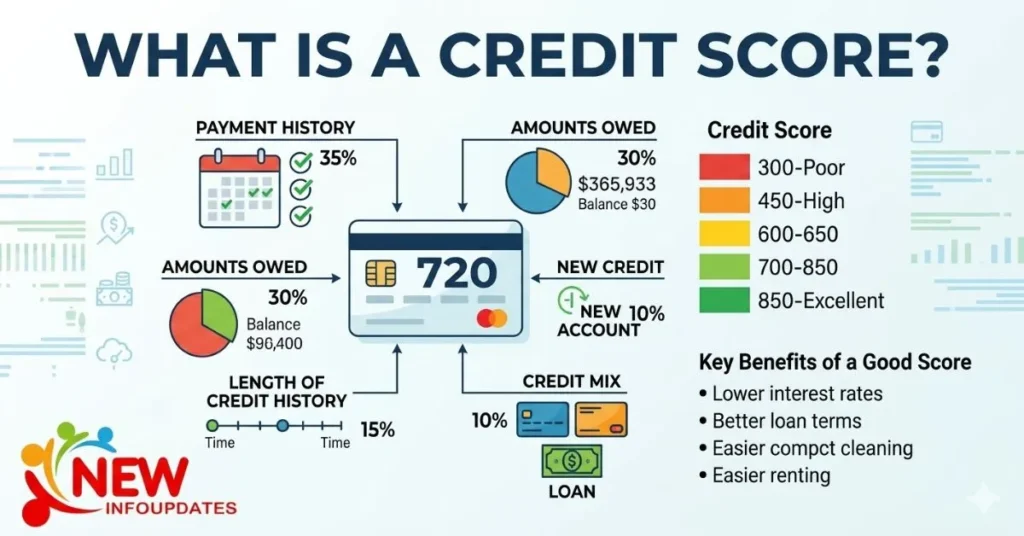

A credit score is a number. It shows how well you handle borrowed money. This number helps banks and lenders decide if they can trust you with loans or credit cards.

The meaning of credit score is simple. It is like a school grade for your money habits. If you pay bills on time, your score can go up. If you miss payments, your score can go down.

Credit scores are used for many things. They can help you:

- Get a credit card

- Buy a car

- Rent a house

- Apply for a loan

- Get lower interest rates

A better score can make borrowing easier.

What Is a FICO Score?

A FICO score is a special type of credit score. It is made by the company Fair Isaac Corporation, also known as FICO. Most lenders use FICO scores when checking credit applications. That is why FICO scores are very important. FICO uses this history to create a score. It looks at different things to decide the number.

One important part is payment history. Paying bills on time is very important because late payments can hurt the score. Another part is credit use. Using too much of a credit card limit may lower the score. For example, if a card limit is $100, spending only a small part is usually better. FICO also checks how long someone has used credit. A longer history can help because it gives more information about money habits. Opening too many new accounts quickly can also lower the score. This may make lenders think a person is borrowing too much money.

A FICO score looks at your money history. It checks things like:

- Payment history

- Credit card use

- Loan history

- Length of credit history

- New credit accounts

Good habits can help your FICO score grow over time.

FICO Score Range

A FICO score range is the group of numbers used to measure how well a person handles borrowed money. A FICO score is very important because banks and lenders use it before giving loans or credit cards. The score helps them decide if a person is careful with money. The company Fair Isaac Corporation created the FICO score system.

Here is the simple breakdown:

- 300 to 579 = Poor

- 580 to 669 = Fair

- 670 to 739 = Good

- 740 to 799 = Very Good

- 800 to 850 = Excellent

A higher score is better. It shows lenders that you manage money carefully.

FICO vs VantageScore

Many beginners also hear about VantageScore. So, what is the difference between FICO vs VantageScore?

Both are credit scoring systems. Both give scores between 300 and 850. Both check your credit habits. But they are created by different companies.

FICO was made by Fair Isaac Corporation.

VantageScore was created by the three main credit bureaus.

The three major credit bureaus are:

- Experian

- Equifax

- TransUnion

Most lenders still use FICO scores more often. But some companies also use VantageScore.

The score numbers may look a little different because each system uses its own formula.

FICO Score and Credit Score

| Feature | FICO Score | Credit Score |

| Meaning | A special type of credit score | A number that shows money habits |

| Created By | Fair Isaac Corporation | Different companies |

| Purpose | Used by many lenders | Used to measure credit health |

| Score Range | Usually 300 to 850 | Usually 300 to 850 |

| Popularity | Most popular scoring system | General name for all score types |

| Used By | Banks, lenders, credit card companies | Banks, lenders, landlords |

| Checks | Payment history, debt, credit use | Similar money information |

| Importance | Very important for loans | Important for borrowing money |

| Example Types | FICO Score 8, Auto Score | FICO, VantageScore |

| Main Goal | Show credit risk | Show financial responsibility |

How Lenders Check Credit

Many people wonder how lenders check credit. Lenders usually contact credit bureaus to see your credit report and score.

Your credit report includes:

- Payment history

- Credit cards

- Loans

- Missed payments

- Credit limits

Lenders use this information to decide if they should lend money to you.

If your score is high, lenders may trust you more. They may offer better loan deals and lower interest rates.

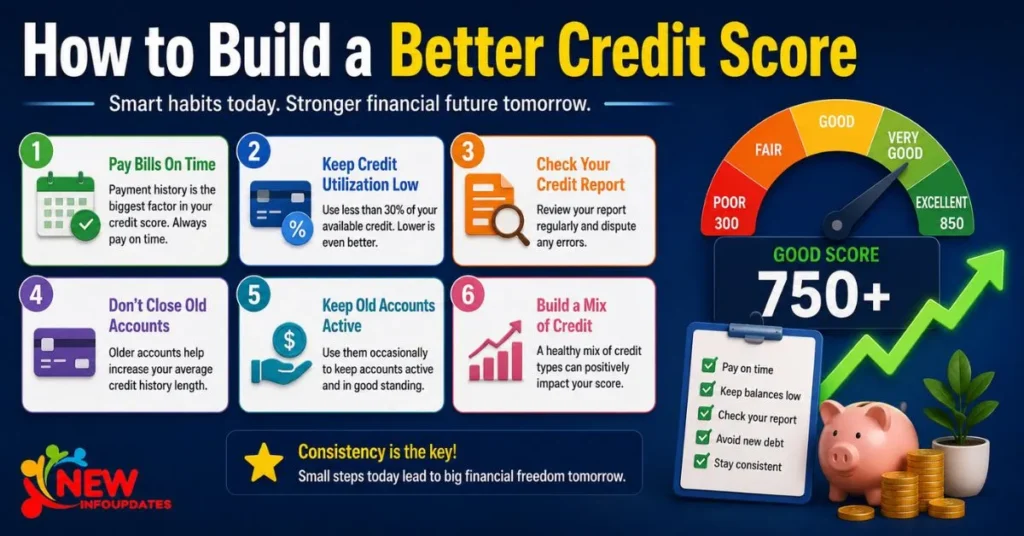

How to Build a Better Credit Score

Building good credit takes time. Small smart habits can help. The best way to build a better credit score is to pay your bills on time. This is very important because late payments can hurt your score. Using too much credit can make lenders worry. Keeping balances low can help your score grow. It is also important not to open too many credit accounts at once. Opening many new accounts quickly can lower your score because lenders may think you are borrowing too much money. Instead, open accounts slowly and only when needed. Checking your credit report is another good habit. Your credit report is a record of your money activity

Here are easy ways to improve your score:

- Pay bills on time

- Keep credit card balances low

- Do not open too many accounts at once

- Check your credit report often

- Use credit carefully

Good habits can slowly raise your score.

Why Credit Scores Matter

Credit scores are important for adults. A good score can help save money and make life easier.

For example, a strong score may help you:

- Get approved faster

- Pay lower interest

- Rent an apartment more easily

- Buy a car with better loan terms

Bad credit can make borrowing harder.

Conclusion

A credit score is a money number. It shows how you handle borrowed money.A FICO score is a type of credit score. Many lenders use it. The good money habits help your score grow and bad habits can lower it. Paying bills on time is very important. Late payments can hurt your score. Higher scores are better. A strong score can help you get loans faster. It can also help you save money. Using too much credit is not good. Small spending is safer. Another factor is credit use. Using too much of a credit card limit may lower the score. For example, if a person has a $100 limit, spending only a small amount is usually better. The length of credit history also matters. A longer history gives lenders more information about money habits. Opening too many new accounts quickly can also lower the score. This guide explains everything in simple words.

FAQ’S

Can too many credit cards hurt my score?

Opening too many cards in a short time can lower your score.

Can I build credit without a credit card?

Yes. Loans, rent reporting, and other credit accounts may also help build credit.