If you’re new to credit, one of the most common questions is: what credit score do you start with? Many beginners assume there’s a default number waiting for them, but the truth is a little different. Understanding your starting credit score can help you make smarter financial decisions and avoid common mistakes early on.

In this guide, we’ll explain what does mean in credit, whether credit scores start at 0, the starting credit score for beginners, how to build credit from no score, the average first credit score, and how long to get first credit score.

What Does Credit Score Mean in Credit?

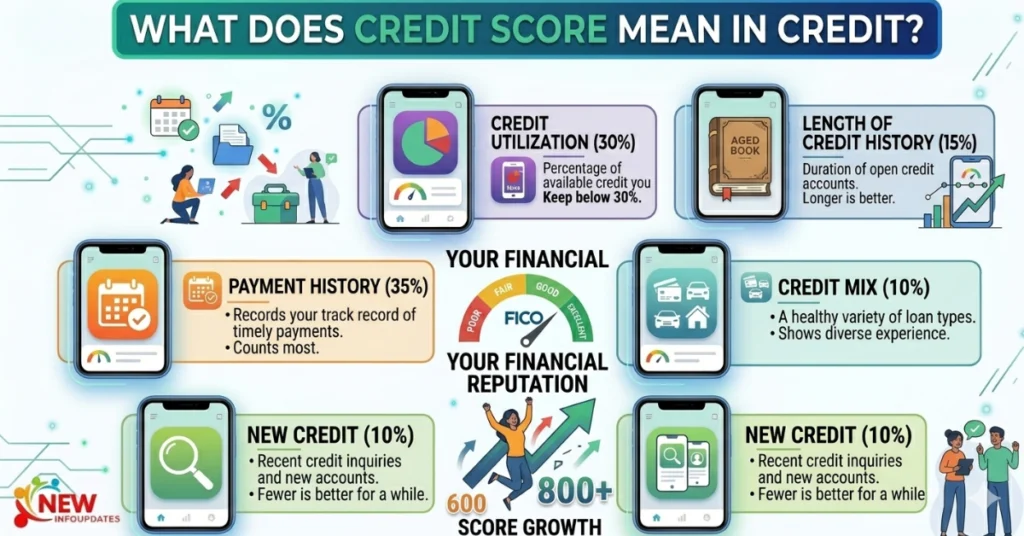

A credit score is a number. It shows how good you are at paying back money you borrow. This number helps banks and lenders decide if they can trust you. In simple words, your credit score means your money trust level. When people ask, “What does credit score mean in credit?” It means they want to know why this number matters. Your credit score tells others how you handle borrowed money. If you pay on time, your score can go up. If you miss payments, your score can go down. Credit is when you borrow money now and pay it later. For example, if you use a credit card, buy something, and pay next month, that is credit. Your credit score tracks how well you do this.

The most common credit score range is:

- 300–579: Poor

- 580–669: Fair

- 670–739: Good

- 740–799: Very Good

- 800–850: Excellent

Your score is based on factors like:

- Payment history

- Credit utilization

- Length of credit history

- Credit mix

- New credit inquiries

In simple terms, your credit score shows how responsibly you manage borrowed money.

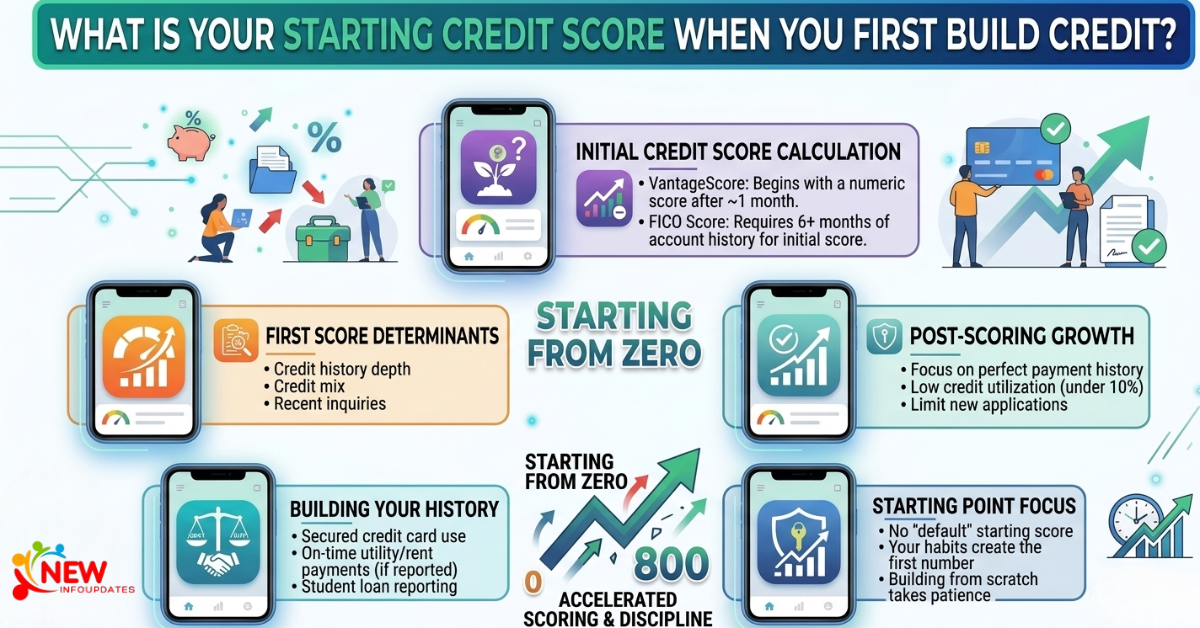

Do Credit Scores Start at 0?

Credit scores do not begin at 0. You do not begin with a score of zero, nor do you automatically receive a starting number like 300 or 600.

Here’s how it actually works:

When you first start building credit, you have no credit score at all because there isn’t enough information in your credit report.

This is called:

No Credit or Thin Credit File

This means:

- You haven’t borrowed enough yet

- Credit bureaus have insufficient data

- There is no score to calculate

So if you’re asking, do credit scores start at 0? — the answer is no. You start with no score, not zero.

What Credit Score Do You Start With?

When you first begin your financial journey, you do not have a credit score at all. Credit scoring systems like FICO and VantageScore need at least one credit account to generate a score. Until then, your file is considered credit invisible or no score available.

Typically:

- FICO Score requires about 6 months of credit history

- VantageScore may generate sooner, sometimes within 1–2 months

Your starting credit score for beginners often lands between 500 and 700, depending on your behavior.

Example:

If you:

- Pay on time

- Keep balances low

- Avoid multiple hard inquiries

Your first score may be in the mid-to-high 600s.

If you:

- Miss payments

- Max out cards

- Apply too often

Your first score may be much lower.

Starting Credit Score for Beginners: What’s Normal?

The starting credit score for beginners isn’t fixed, but many first-time users see scores around:

Average Range:

630 to 690

This can vary depending on:

- Type of first account

- Payment habits

- Credit card balance

- Student loans or authorized user accounts

Important:

Your first score is not permanent. It can rise or fall quickly based on your early habits.

Average First Credit Score: What Most People See

The average first credit score is usually considered to be in the mid-600s, especially for those who start with a secured credit card or student credit card and make on-time payments.

Common beginner scenarios:

Secured Credit Card:

- Often first score: 650–700

Student Credit Card:

- Often first score: 630–690

Authorized User on Parent’s Card:

- Could start even higher depending on account history

Your initial score depends less on age and more on how your first accounts are managed.

How Long to Get Your First Credit Score?

Another big question: how long does it take to get your first credit score?

FICO:

Usually 6 months after opening your first credit account

VantageScore:

Can appear in as little as 30–60 days

Timeline Example:

Month 1: Open secured card

Month 2: First reported payment

Month 3: VantageScore may appear

Month 6: FICO score likely generated

So, if you’re wondering how long to get your first credit score, expect around 3–6 months.

How to Build Credit From No Score

If you currently have no score, don’t worry. Learning how to build credit from no score is easier than many people think.

1. Open a Secured Credit Card

A secured card requires a refundable deposit and is one of the easiest ways to start.

2. Become an Authorized User

Join a trusted family member’s credit card account.

3. Credit Builder Loan

Some banks and credit unions offer loans specifically designed to build credit.

4. Pay Bills On Time

Payment history is the biggest factor in your score.

5. Keep Utilization Low

Try to use less than 30% of your available credit.

Best Beginner Strategy for Fast Credit Growth

To build a strong starting credit score, follow this plan:

Month 1:

- Get a secured card

- Make one small purchase

Months 2–6:

- Pay balance in full

- Keep utilization under 10%

- Avoid unnecessary applications

After 6 Months:

- Check FICO score

- Consider upgrading to unsecured credit card

Common Mistakes Beginners Make

When learning how to build credit from no score, avoid these errors:

Missing Payments

Even one late payment can hurt badly.

Maxing Out Cards

High utilization lowers scores quickly.

Applying Too Often

Multiple hard inquiries can signal risk.

Closing First Card Too Early

Length of history matters.

Can You Start With Good Credit?

Yes it’s possible.

If you become an authorized user on a parent’s well-managed account, your average first credit score may start higher than someone building from scratch.

However, independently, most beginners must earn their score over time.

Final Thoughts

It start with no credit score. You build trust with smart money choices. Pay every bill on time. Good habits help credit grow. In the beginning, you usually start with no credit score at all. This happens because credit companies need time to learn about your money habits. It is like starting school before getting your first report card. You need to do some work first before a grade can be given. Credit works the same way. When you first use a credit card, pay a loan, or borrow money and pay it back, your credit history begins to grow. After about 3 to 6 months, a credit score may be created. This score is based on how well you use credit.

The key is consistency:

- Pay on time

- Keep balances low

- Be patient

For beginners, understanding what does mean in credit and learning how to build credit from no score can set you up for better loans, lower interest rates, and greater financial freedom.

FAQS

Can your first credit score be excellent?

It’s uncommon, but possible if you’re added as an authorized user to someone with a long, positive credit history.

Can I have a credit report without a credit score?

Yes. You may have a credit report showing account activity, but if there isn’t enough recent information, you may still not have a score yet.

Does age affect your starting credit score?

No. Your age alone doesn’t determine your score, your credit activity and payment behavior do.

Should beginners apply for multiple credit cards?

Usually no. Too many applications can create hard inquiries and may lower your score temporarily.